When you leave your job, you are paid a full-and-final settlement by your employer. This settlement comprises of your salary, the allowances, payments, and reimbursements you’re eligible for, and gratuity assuming you’ve served your employer for five years or more.

Gratuity is a lump sum paid to you for your continued service. It’s a useful sum to receive, especially for anyone who’s served a particularly long stint with their employer. It can be put to several uses such as contribution to your retirement kitty, paying off a loan, or funding your child’s education.

Let’s understand how gratuity works as a concept.

What Is Gratuity?

Gratuity is a lump sum you receive when leaving your employer after at least five years of continuous service by resigning, retiring or superannuation. Eligible employees are also entitled to gratuity on their death or disablement due to accident or disease. However, in such a case, the five-year requirement isn’t applied.

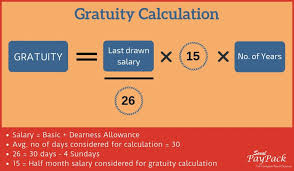

How Gratuity is Calculated?

The gratuity payment rules are governed by the Payment of Gratuity Act 1972. There are a different set of rules applied for organizations covered under this Act and for organizations that are not. As per the law, every individual working in a shop or an establishment which has 10 or more employees on any day of the preceding 12 months is entitled to gratuity. A shop or establishment where the Act is applicable will have to provide gratuity even if the number of employees falls below 10.

There is a simple formula through which gratuity is calculated.

Employees Working In Organisation Covered Under The Payment Of Gratuity Act 1972

Gratuity = (Last drawn salary x number of service years x 15) / 26. The last drawn salary comprises basic and dearness allowance (DA).

Let us understand this with the help of an example. If your last drawn salary is Rs. 80,000, which includes your basic and DA) and you have worked in the organization for seven years and four months, then your gratuity will be 15 x 80000 x 7 / 26 = 3,23,076.92. Do note that the number of months below five is rounded off to that year, whereas months above five are rounded off to the next year.

Employees Working In Organisation That Are Not Covered Under The Payment Of Gratuity Act 1972

Gratuity = (Last drawn salary x number of years completed in service x 15) / 30.

In the above example, the gratuity will be calculated as 15x 80000 x 7 / 30 = 2,80,000.

For calculation of gratuity for employees not covered through the Act, the working years are taken as actual years completed.

Taxation of Gratuity

If you are a government employee, the gratuity received will be fully tax exempted. For non-government employees, the least of the following is tax-exempted: gratuity calculated, actual gratuity you receive or Rs. 20 lakh, whichever is lower. Any amount above this will be taxed as per the tax slab of the employee.

How To Use Gratuity Amount

It would be wise to use to your gratuity money for savings and achieving financial goals. You may also use it to settle your debts such as credit card dues or home loan to reduce your loan burden. Since it is your hard-earned money, you can consider investing in safe options that assure capital safety such as fixed deposits or PPF. Investing in the government-backed gold schemes at this juncture may also give good returns. Before you decide on investing your gratuity purse, you can take the help of a financial advisor.