Reserve Bank of India (RBI) on last Wednesday raised the interest rate by 50 basis points to a two-year high of 4.9 per cent as it doubled down to tame inflation that has surged in the last couple of months.

Reserve Bank of India (RBI) on last Wednesday raised the interest rate by 50 basis points to a two-year high of 4.9 per cent as it doubled down to tame inflation that has surged in the last couple of months. All the six members of the Monetary Policy Committee (MPC), headed by RBI Governor Shaktikanta Das, unanimously voted for the latest rate hike. Amid rising interest rates, a Knight Frank India report explains how rising interest rates will impact home buyer’s affordability.

“The real estate sector has been on a strong recovery path after surviving the worst of the pandemic. Annual residential sales in 2021 have reached within striking distance of 2019 volumes and recent monthly sales trends also show strong momentum. This has largely been driven by extremely low interest rates which supported homebuyer demand. However, sharp rise in inflation has forced the central bank to raise interest rates and suck out excess liquidity in the market. While it is a critical tool in the fight against the burgeoning inflation, this turn in the interest rate cycle could be a significant headwind to real estate demand,” Knight Frank India report said.

Read More: Trehan Group to invest Rs 125 crore in new housing project at Neemrana

Cumulative REPO Rate hike of 90 basis points

“The 50-bps hike in the REPO rate in June Monetary Policy Committee (MPC) announcement comes on the back of a 40-bps increase in May. Further, the significant 1 percentage point increase in the FY23 consumer inflation estimate to 6.7%, which is higher than RBI’s upper tolerance band of 6%, also suggests that further rate hikes are likely. The RBI is likely to continue increasing the policy rate to narrow the gap between consumer inflation and repo rate and reduce the extent of negative real interest rate in the economy, which still stands at -1.8%,” the report added.

“While home loan interest rates are still well below pre-pandemic levels, it is worthwhile to gauge the impact of every increase in the home loan rate on the EMI load and eventual affordability levels of the end consumers,” it further adds.

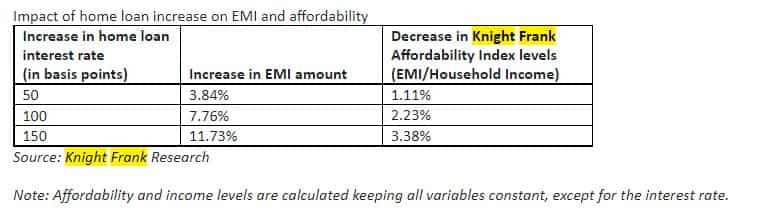

“Home loan rates are still approximately 150 bps below those prevailing in 2019 and a reversion to those levels will result in an 11.73% increase in the EMI load for the homebuyer and an effective 3.38% decrease in affordability basis the Knight Frank Affordability Index. This analysis does not account for change in income levels or house prices and considers interest rates as the only variable. House price levels have increased over the past 12 months across most markets and should also have a material impact on affordability,” the report said.

Read More: Around 4.8 lakh homes worth Rs 4.48 lakh crore stuck or delayed in top 7 cities

AVERAGE FOR BENGALURU

“Even while basis the home loan terms of individual homebuyers there will be varying level of lender response measures, the increase in Repo Rate earlier during May and now in June, will make EMIs costlier for buyers. With the increase in home loan interest rate during May and now in June, EMIs have increased for the borrower. For instance, assuming complete transmission of repo rate increase, for a home buyer in Bengaluru with a home loan of INR 75 lacs, the EMI has increased from INR 59,962 per month before the rate hike to INR 61,803 in May and now INR 64,141 in June,” Knight Frank India report said.

AVERAGE FOR NCR

“Even while basis the home loan terms of individual homebuyers there will be varying level of lender response measures, the increase in Repo Rate earlier during May and now in June, will make EMIs costlier for buyers. With the increase in home loan interest rate during May and now in June, EMIs have increased for the borrower. For instance, assuming complete transmission of repo rate increase, for a home buyer in NCR with a home loan of INR 1 crore, the EMI has increased from INR 79,949 per month before the rate hike to INR 82,404 in May and now INR 85,521 in June,” Knight Frank India report added.

AVERAGE FOR MUMBAI

“Even while basis the home loan terms of individual homebuyers there will be varying level of lender response measures, the increase in Repo Rate earlier during May and now in June, will make EMIs costlier for buyers. For instance, assuming complete transmission of repo rate increase, for a home buyer in Mumbai with a home loan of INR 2 crore, the EMI has increased from INR 159,898 per month before the rate hike to INR 164,807 in May and now INR 171,041 in June,” Knight Frank India report.

“In practical terms, the increase in home loan rates usually translates to an increase in tenure rather than an actual increase in EMI, effectively subduing its impact to some extent. While steep, the interest rate hikes are not a surprise and have been factored into the market sentiment which continues to hold strong. We do not believe that home loan rates approaching 2019 levels will be enough to subdue market momentum significantly. The performance of the broader economy will have a greater bearing on market momentum for the remainder of the year as it dictates homebuyer income levels and demand much more directly. As things stand currently, the RBI having kept the FY23 GDP growth estimate constant gives credence to our belief that residential demand should not be impacted materially in 2022,” the report concluded.

(Disclaimer: The views/suggestions/advice expressed here in this article are solely by investment experts. Zee Business suggests its readers to consult with their investment advisers before making any financial decision.)