The Systematic Withdrawal Plan or SWP is a facility provided to Mutual Funds investors through which they can withdraw a fixed amount for a specified period.

Systematic Withdrawal Plan: Systematic Investment Plan (SIP) is one of the most popular facilities in Mutual Funds, but did you know mutual funds can also help generate regular income? The Systematic Withdrawal Plan (SWP) facility in Mutual Funds helps investors get a regular income from their investments. Let’s take a look at what a Systematic Withdrawal Plan is and how it works.

Read More: NPS calculator: How to get ₹2.94 lakh monthly pension by ₹12500/month NPS contribution — explained

What is a Systematic Withdrawal Plan?

The Systematic Withdrawal Plan or SWP is a facility provided to Mutual Funds investors through which they can withdraw a fixed amount for a specified period.

According to Shweta Rajani, Head, Mutual Funds, Anand Rathi Wealth Limited, SWP allows an investor to withdraw money from Mutual Fund at predetermined intervals (i.e., yearly, monthly, weekly, or daily). This option is mostly opted for by retired individuals. It helps to have a steady flow of income from their investments.

How does the Systematic Withdrawal Plan work?

Investors can avail the benefit of SWP but should know that it affects their mutual fund account because the value of the fund is reduced by the number of units withdrawn. Anyone can start SWP; here is how to do it:

– An investor has to select the mutual fund scheme and decide on the frequency and amount of frequency.

-On a specified time, the Asset Management Company (AMC) will sell units from investors holding in the scheme to generate the required amount of cash for the withdrawal.

– AMC will transfer the amount to the investor’s account. This process will continue until the investor decides to stop, modify, or the number of their units becomes zero.

When to start a Systematic Withdrawal Plan?

According to Shweta, an investor should opt for SWP in the following situation:

-For generating regular income

-When an investor is looking to diversify income sources

-Managing retirement income

Why opt for a Systematic Withdrawal Plan?

Investors can opt for SWP for the following reasons:

-To create a source of regular income

– It helps in capital preservation as one can avoid selling all the units at once instead of opting for withdrawal in a systematic fashion.

– It helps an investor diversify the sources of income while investing in equity, which can help beat inflation.

– It also provides flexibility to withdraw. An investor can choose the amount and frequency of withdrawals.

-SWP is better than the dividend option and brings in tax efficiency.

Systematic Withdrawal Plan: Calculation

To put things into perspective, if an investor has 10,000 units in a mutual fund scheme and wants to withdraw Rs 5,000 monthly through the Systematic Withdrawal Plan, let us assume the Net Asset Value (NAV)—the net value of an investment fund’s assets less its liabilities, of the scheme is Rs 10.

The withdrawal of Rs 5,000 from this scheme will mean that 500 units are being sold, which is Rs 5,000/NAV of Rs 10. The remaining units in your mutual fund after this withdrawal will be 9,500 units (10,000-500).

Suppose in the next month, the NAV of the scheme increases to Rs 20, then the withdrawal of Rs 5,000 would mean selling 250 units, which is Rs 5,000/NAV of Rs 20. The mutual fund would be left with 9,250 units post this withdrawal (9,500-250). So, with each withdrawal, the mutual fund will see a decline in its units.

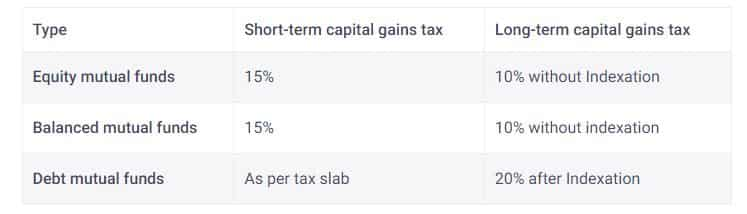

Systematic Withdrawal Plan: Tax benefit

According to Anup, SWP is tax-efficient.

“When one begins an SWP from a debt fund, any capital gains made in the first two years of investment will be considered short-term capital gains and taxed accordingly. However, if one continues SWP for more than three years, any gains made after the third year will be treated as long-term capital gains and taxed at a lower rate.”

Also, no tax is deducted at source for investors while withdrawing the SWP amount. Here is a quick look at the capital gains tax for different types of mutual funds: