A higher credit score generally indicates a lower risk borrower, while a lower credit score may result in a higher interest rate or even the denial of a loan.

A credit score-based home loan refers to a mortgage loan that is approved or offered based on the borrower’s credit score. This score is generated using data from credit history of an individual. It is nothing but a numerical representation of an individual’s creditworthiness.

Also Read- Nominee not mentioned? Here’s how to withdraw EPF money after member’s death

When a borrower applies for a home loan, lenders evaluate creditworthiness to determine the risk of lending money. They use credit score, along with other factors such as income, employment history, and debt-to-income ratio, to assess ability to repay the loan. A higher credit score generally indicates a lower risk borrower, while a lower credit score may result in a higher interest rate or even the denial of a loan.

Lenders typically have their own credit score requirements and may set minimum thresholds for borrowers to qualify for specific loan programs. For example, some lenders might give loans to anyone having a credit score of 700, while others might reject the same. It may vary from lenders to lenders.

Read More: How to apply for a minor’s PAN Card? Procedure and documents required

Having a higher credit score can offer several advantages when applying for a home loan. It can increase your chances of loan approval, help you secure a lower interest rate, and potentially save you money over the life of the loan. On the other hand, a lower credit score may make it more challenging to obtain a loan or result in less favourable loan terms.

It’s important to note that credit scores are not the sole factor considered in the loan approval process. Lenders also review other aspects of your financial profile, such as your employment history, income stability, and the amount of debt you currently carry.

Read More: PM-Kisan Scheme: How To Apply For 14th Installment? Here’s The Step-By-Step Guide

To improve your chances of obtaining a home loan with favourable terms, it’s advisable to maintain a good credit score by paying bills on time, reducing debt, and avoiding new credit inquiries or opening multiple new credit accounts. Regularly monitoring your credit report for errors or inaccuracies is also recommended, as these issues can negatively impact your credit score.

Remember that specific lenders may have their own policies and criteria regarding credit scores and home loans, so it’s always a good idea to shop around, compare offers, and consult with multiple lenders to find the best loan options available to you.

Also Read– Senior Citizen Savings Scheme: 5 Advantages And Disadvantages Of Investing In SCSS

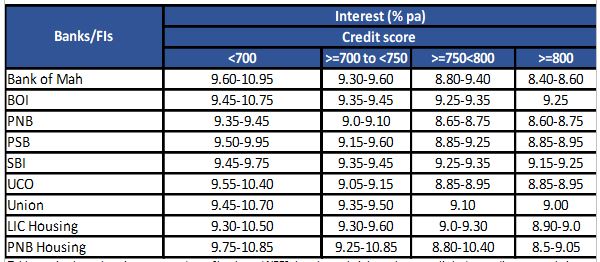

The table below compares the home loan interest rates of some lenders for customers holding 700 or higher credit scores. You can compare and decide as per your requirements.

Home loan interest rates corresponding to credit scores

Read More: Cheapest Home Loan Options For You To Own A House

Note: The table consists home loan interest rate data of banks and NBFCs that shows their home loan rate linked to credit score on their website. Interest rate is indicative and in actual situation the rate may vary depending on various factors and the bank’s T&C. Data as on 11 April 2023.