As NRIs explore ways to secure their hard-earned money and wish to get good returns on their investments, Non-Resident Ordinary (NRO) fixed deposits (FDs) could be a rewarding financial instrument.

Are you an NRI looking to park your funds for stable returns in India? Although there are many options to invest your money, however, if you are looking for good returns without risks, then you can opt for a fixed deposit instrument specifically meant for NRIs.

Read More: Aiming For Rs 1 Lakh Pension After Retirement? Here’s How To Do It

As NRIs explore ways to secure their hard-earned money and wish to get good returns on their investments, Non-Resident Ordinary (NRO) fixed deposits (FDs) could be a rewarding financial instrument.

NRO FDs are a type of bank deposit offered to NRIs by Indian banks. These deposits can be made in Indian rupees and are maintained for a fixed tenure, ranging from a few months to several years. The interest rates offered on NRO fixed deposits are competitive and often higher than those in many other countries, making them an attractive investment option for NRIs seeking stable returns.

One of the primary benefits of NRO fixed deposits is the assurance of safety and security. Banks in India are well-regulated and supervised by the Reserve Bank of India (RBI), providing NRIs with peace of mind about their funds’ safety. Additionally, the interest earned is fully repatriable, ensuring that NRIs can easily take this money back to their country of residence.

Another compelling aspect of NRO fixed deposits is the flexibility they offer in terms of tenure and interest payment options. NRIs can choose the duration of their fixed deposit based on their financial goals, be it short-term or long-term.

NRO fixed deposits also serve as a cushion against currency fluctuations. Since the deposits are held in Indian rupees, NRIs are safeguarded from the impact of volatile exchange rates. This feature becomes particularly significant during periods of economic uncertainty when exchange rates can fluctuate drastically, potentially eroding the value of investments denominated in foreign currencies.

Additionally, NRO fixed deposits act as a crucial bridge between NRIs and their families in India. Many NRIs have financial commitments, such as educational expenses, medical bills, or supporting their loved ones back home. By investing in NRO fixed deposits, NRIs can ensure a steady source of income or a lump-sum amount at maturity to fulfill these responsibilities.

Moreover, NRO fixed deposits play a pivotal role in fostering a sense of financial discipline among NRIs. With predetermined tenures and penalties for early withdrawals, these deposits encourage NRIs to cultivate a habit of saving and investing for the long term. This financial discipline can have far-reaching benefits beyond the NRO fixed deposit, impacting other aspects of their financial planning and management. Despite the numerous advantages, NRIs must be aware of the tax implications associated with NRO fixed deposits.

Read More: Aiming For Rs 1 Lakh Pension After Retirement? Here’s How To Do It

NRO fixed deposits have emerged as a reliable and rewarding investment option for NRIs, providing them with a steady pillar of financial security. However, NRIs must carefully consider the tax implications to optimise their investment decisions effectively.

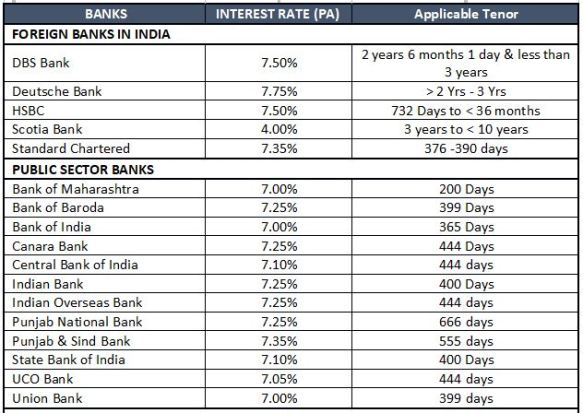

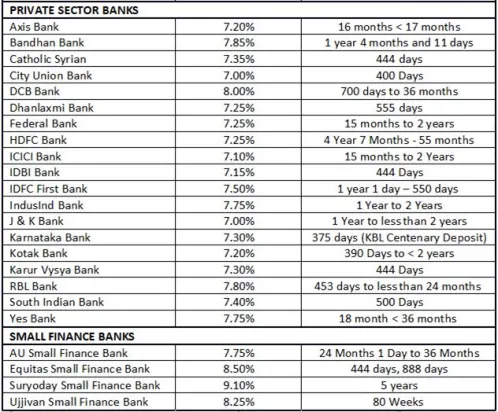

The table below compares the interest rates of around forty banks and applicable tenures. NRIs can compare and take a decision based on their requirements and financial goals.

INTEREST ON NRO DEPOSITS (Best Offered Rate & Applicable Tenor)

Note: Data as on respective banks’ website on 25 July 2023. Highest Interest rate offered on NRO deposits of up to Rs 2 Cr for tenor up to 5 years for all listed (BSE) public & private banks, and foreign banks considered for data compilation. Highest rate offered for up to 5-year (7 days to 5 years) period is considered in the table. Banks whose websites don’t mention the data are not considered.