Given the upward trajectory of short-term rates, employing a laddering strategy for short-term deposits can be particularly advantageous.

As State Bank of India has increased short-term fixed deposit rates by 25 to 75 basis points, a move likely to be followed by other banks, individuals should now adopt a laddering strategy for deposits up to one year. There would be a clamour for short-term deposits with the one-year bank fixed deposit rates nudging higher, and longer-term rates possibly remaining flat.

Read More: Reliable Monthly Income: Is This Post Office Scheme Better For You? Know Features Now

Individuals should divide the amount and invest in varying maturities, instead of putting the entire amount in a single deposit. Lenders having high loan-to-deposit ratios may increase their short-term deposit rates to attract fresh money for funding their credit growth.

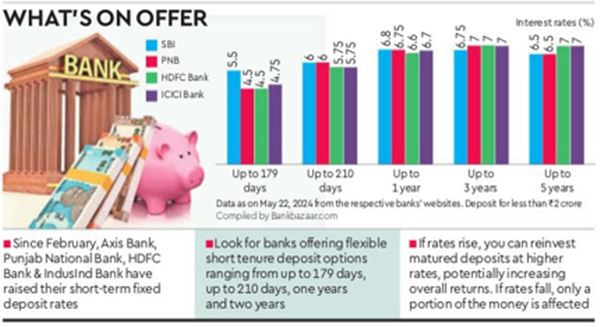

Since February, banks such as Axis Bank, Punjab National Bank, HDFC Bank, and IndusInd Bank have increased their short-term fixed deposit rates. So, given the upward trajectory of short-term rates, employing a laddering strategy for short-term deposits can be particularly advantageous. In fact, this will enable reinvestment opportunities whenever there is a chance to secure higher interest rates. Individuals should look for banks offering flexible short tenure options ranging from up to 179 days, up to 210 days, one years and two years. This strategy will help maximise returns over time, provide liquidity at regular intervals and reduce the risk of being locked into a single rate for a long period.

Adhil Shetty, CEO, Bankbazaar.com, says laddering fixed deposits will benefit investors from changing interest rates. “If rates rise, you can reinvest matured deposits at higher rates, potentially increasing your overall returns. Conversely, if rates fall, only a portion of your money is affected, as the longer-term deposits were locked in at higher rates earlier.”

Read More: SBI sets out to make infra loans costlier

Higher yields

Short-term deposits have tenures ranging from seven days to one year. They are ideal for investors looking to park their funds for a brief period while earning better returns than a regular savings account. These deposits offer flexibility and are suitable for meeting immediate financial goals or emergencies.

In fact, individuals must note that for a few banks, the interest rates for one-year deposits are higher than longer tenure of three and five years. Individuals can open short term bank deposits to park their short-term surpluses provided the rates offered for such deposits are attractive.

Investors should also compare the savings account interest rates offered by small finance banks and some private sector banks, especially those offering interest rates slabs of 5-7%. Such high-yield savings accounts will offer higher liquidity and flexibility than short-term bank deposits.

Special deposits

Many banks have introduced deposits for specific durations. These might offer higher interest rates for particular tenure periods, such as 444 days or 999 days, or during festive seasons to attract more deposits. Investors can benefit from these schemes by locking in higher rates for a specified period. However, they will have to keep in mind that premature withdrawal is not possible in such deposits.