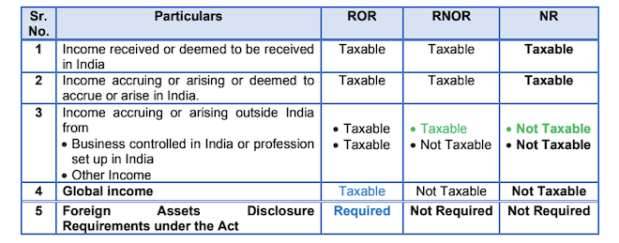

Income which is accruing or arising or deemed to accrue or arise in India is also taxable in the hands of all types of assesses, whether it be ROR, RNOR or NR.

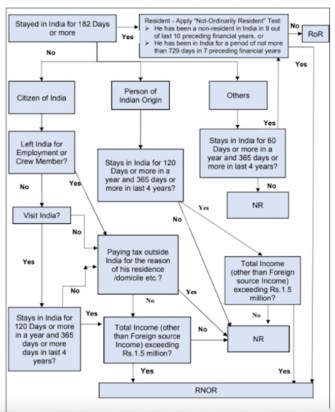

All resident individuals in India are required to pay tax on their income if it is above the basic exemption limit. According to a recent research report – ‘Salary Income: Tax Incidence and Optimisation‘ – published by RSM India, a tax consultancy firm, an individual is treated as a Resident of India in a financial year if s/he satisfies the following basic conditions:

First, s/he is in India for a period of 182 days or more in that financial year, or

Second, s/he is in India for 60 days or more during that financial year and has been in India for 365 days or more during last 4 years.

The report says that the above basic conditions are relaxed in the case of the following persons:

a) An Indian citizen who leaves India in any year for the purpose of employment or as a member of the crew of an Indian Ship

b) An Indian citizen or a person of Indian origin who resides outside India and who comes to India on a visit and whose total income (excluding income from foreign source) is up to Rs.15 lakh (1.5 million). Here the person of Indian origin means the person or either of his parents or either of his grandparents were born in undivided India.

The above-mentioned persons shall be treated as residents only if their total period of stay in India exceeds 182 days or more in the relevant financial year (i.e. 60 days shall be replaced as 182 days in the 2nd basic condition for determining whether a person is resident in India).

Read More: Income Tax department operationalises e-advance ruling in Delhi, Mumbai

Resident and Ordinary Resident (ROR) vs Resident but Not Ordinarily Resident (RNOR)

The report further says that with effect from 1 April 2020, the 60 days limit has been replaced by 120 days in the second basic condition for an Indian citizen or a person of Indian origin who comes to India on a visit and whose total taxable income (other than income from foreign sources) is above Rs 15 lakh.

“As such, under the second basic condition, he will be considered as resident if he stays in India during the relevant financial year for 120 days or more and 365 days or more in the preceding 4 financial years and his Indian taxable income exceeds Rs. 1.5 million,” the report says.

However, if such person (having above Rs 15 lakh taxable income) stays in India during the relevant financial year for 120 days but less than 182 days then s/he shall be treated as Resident but Not Ordinarily Resident (RNOR) and his global income will not be subject to tax.

Further, if an individual does not satisfy any of the basic conditions altogether, s/he will be treated as a non-resident of India (NR) for that financial year.

In case an individual satisfies any of the basic conditions and is treated as a Resident then it is necessary to determine whether he is a “Resident and Ordinary Resident (ROR)” or “Resident but Not Ordinarily Resident in India (RNOR)”. For this purpose, the report says the person is required to check if s/he satisfies any one of the additional conditions listed below:

- He has been a non-resident in India in 9 out of last 10 preceding financial years; or

- He has been in India for a period of not more than 729 days in 7 preceding financial years; or

- An Indian Citizen or a person of Indian origin whose total income (other than income from foreign sources) exceeds Rs. 1.5 million during the financial year and who has been in India for a period of 120 days or more but less than 182 days; or

- An Indian Citizen who is deemed to be resident in India as per new Section 6(1A).

“If he fulfills any of the above conditions, he will be considered as RNOR. If he fails to satisfy all the above conditions, then he will be treated as ROR,” the report says.

Read More: BIG! Now Lower Tax On Rent-Free Accommodation From Employer? Income Tax Dept Notifies Rules

Deemed Resident under Section 6(1A) of Income Tax Act

Section 6(1A) of the Income Tax Act, which provides for “Deemed Resident” is applicable from the financial year commencing from 1 April 2020.

“An Individual being a Citizen of India having total Indian Income (i.e. income other than income from foreign sources) exceeding Rs 1.5 million, shall be deemed to be resident of India in any financial year, if he is not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature. However, such a person shall be treated as Resident but Not Ordinarily Resident (RNOR) and his entire global income will not be subject to tax,” the report says.

Who is liable for tax?

The Finance Act, 2021 has defined the term “Liable to tax” in relation to a person and with reference to a country. It means that “there is an income-tax liability on such person under the law of that country for the time being in force and shall include a person who has subsequently been exempted from such liability under the law of that country,” the report says.

The following flowchart provides an overview of the determination of Residential status:

Taxability of Income

A resident and ordinary resident is taxable in respect of his global income. Therefore, if an expatriate executive becomes resident and ordinary resident, then he will be taxable in India on his global income.

Income which is accruing or arising or deemed to accrue or arise in India is also taxable in the hands of all types of assesses, whether it be ROR, RNOR or NR.

Income received would constitute Income received for the first time. Thus, in case of any income which is received outside India but is subsequently remitted to India, the same would not constitute as receipt of Income.

Any income which is taxed on accrual basis and subsequently remitted to India would not be chargeable to tax at the time of remittance.

Salary income shall be deemed to accrue or arise in India, if the income is earned in India. In the following cases, salary income shall be regarded as earned in India only if the salary is payable for:

- service rendered in India; and

- the rest period or leave period which is preceded and succeeded by services rendered in India and forms part of the service contract of employment.

- The following incomes shall be deemed to be received in India-

- Annual accretion to the credit of Recognised Provident Fund (RPF) in the nature of contribution in excess of 12% pa of salary to RPF or interest in excess of 9.5% pa;

- Transfer of amount from unrecognised provident fund to recognised provident fund;

- Contribution made, by Central Government or any other employer to the account of an employee under a pension scheme referred to in section 80CCD.

Disclaimer: The above content is for informational purposes only. The facts and explanations mentioned above are those of RSM India’s report and do not reflect the views of financialexpress.com. Please consult your tax advisor for any tax-related queries.